Why the Economy is Worse than it Looks

The numbers say we're at the cliff

There are countless indicators pointing to recession in early 2024, but most economists are now completely ignoring them, forecasting more growth along with interest rate cuts at the Fed. It’s hard to blame them, since many of these recession indicators were flashing red back in January and we’re still waiting for the crash.

The key here that everybody is missing lies in the very data being dismissed – a classic case of not seeing the forest for the trees. If we do a quick dive through the labor market numbers, it helps pull the curtain back and expose what’s really going on.

Put simply, we’ve never recovered from the government lockdowns that began in 2020. The labor market shows, by at least five different measures, that we’re way below trend – an important thing to consider while everyone is so concerned about levels.

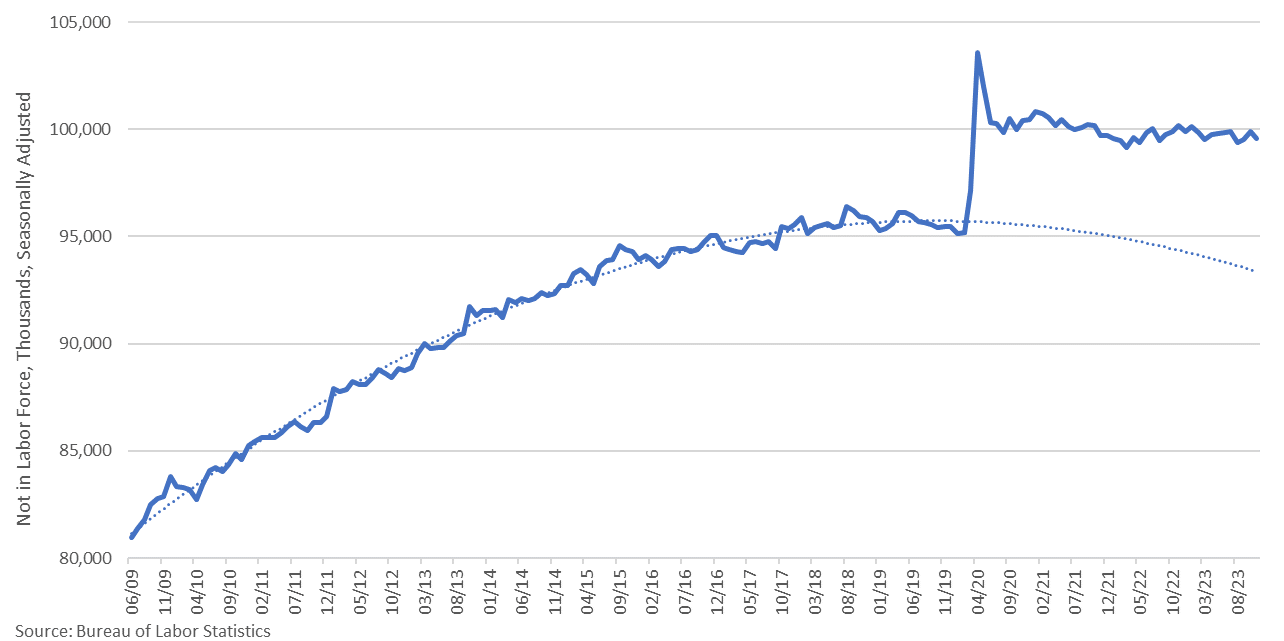

Even after the lockdowns ended, millions of people never returned to the labor force. Before that, the trend of those categorized as “not in the labor force” had been trending down. Today, the gap is millions of people.

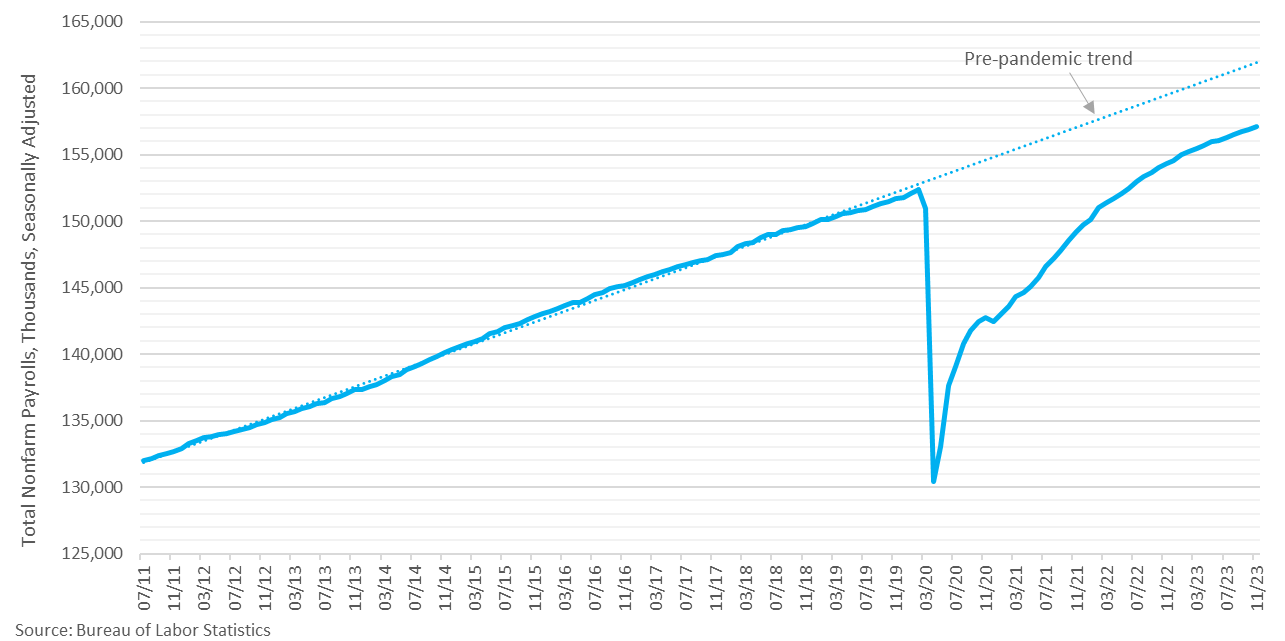

Likewise, we see similar sized gaps with the employment-to-population ratio, the employment level from the household survey, and the number of nonfarm payrolls from the establishment survey.

This data affects both the numerator and denominator in the unemployment rate calculation, yielding a modified rate between 6.1% and 6.8% because it accounts for the missing 4.3 to 5.5 million people absent from the official calculation.

Suddenly, the very bad forward-looking indicators we see all around make perfect sense. Let’s say the data point to a 2-percentage-point rise in the unemployment rate over the next year. We’re not talking about the unemployment rate going from 3.7% to 5.7%.

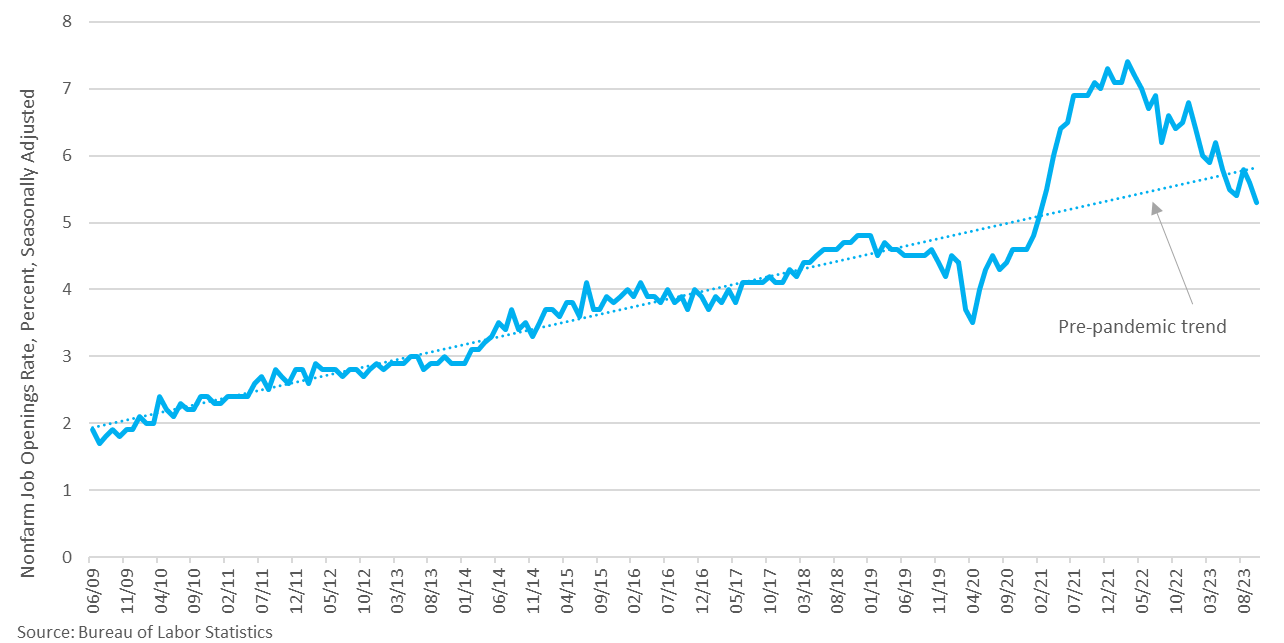

Instead, we’re looking at going from maybe 6.5% to 8.5%. And we see exactly the same thing with the level and rate of job openings, which show labor demand too has softened below its pre-pandemic trend.

And we’ve also seen a boon in government jobs, which, although unsustainable, is goosing the headline jobs numbers. Once again, a little context goes a long way here in interpreting the data more accurately.

And with that context, the very negative indicators from the regional Federal Reserve banks, purchasing manager indexes, as well as countless reports from the Census Bureau, BEA, and BLS (and just about every other three- or four-letter agency), all make much more sense.

The problem is not with the data and where it shows the labor market is heading, the problem is with our perception of where we stand today.

The increasingly prevalent belief among economists and talking heads alike is that we’re much further along than we actually are. The labor market - especially the private sector - is nowhere near its pre-pandemic trend.

To be clear, economies in recent history often don’t return to their pre-recession trends, even in a strong recovery, but 2020 was not a normal recession.

Coming out of one of those normal recessions, the initial growth is barely positive but then picks up steam. 2020 was exactly the opposite - it started with record growth and then slowed.

That makes sense because it was such an abnormal economic contraction - entirely artificial and imposed by government fiat.

That leaves us with a labor market much more anemic than most economists perceive it to be.

But the point here is not to highlight the labor market as an outlier but to say that it’s emblematic of the economy at large. We’ve never really recovered from 2020 and 2021. We already had two consecutive quarters of negative economic growth in 2022 (used to be called a recession).

And the last GDP report pulled a huge amount of growth forward from next year through inventory buildup. GDI has fallen behind GDP at rates never seen before.

In short, the economy is not rip-roaring along like it was in 2019. The very negative indicators we’re seeing are in the context of a relatively negative current situation. That means things are poised to get worse, but perhaps not much worse than they already are.

It’s like being just one or two steps up on a flight of stairs before you trip and fall down, compared to being all the way at the top of the staircase. You tripped and fell down to the same landing either way, but one fall relatively worse than the other.

So, don’t ignore all the indicators – the numbers don’t lie. But we have to be able to interpret them honestly, not politically, not with rose-colored glasses, not with pessimism or optimism.

It’s reminiscent of the saying that the economist is the one most in touch with reality because he sees the world not as he wants it to be, not as it could be, and certainly not as it should be – but as it is.

Completely subjective 👎🏼

Your outlook is exceedingly negative based on a few obscure indicators. Plus, the new post-pandemic trend lines are steeper than the pre-pandemic ones, indicating we are in our way back to the levels that were in reach before. Your point about trend lines basically ignores the new trend line, and just relies on the old one, as if it’s the pre-ordained “correct” one that all future trends should soring back to immediately. Any time period in question will produce its own unique trend line, your choice of trend line was completely arbitrary.