The Fed Is Abusing Its Own Made-Up Accounting Rules

How Powell & Co. are preventing a run on the Standing Repo Facility, adding liquidity, and reaccelerating inflation

Some funky things have been going on at the Federal Reserve, in sovereign debt markets, and with reserve balances. Markets have not been responding the way they “should,” but it turns out there are good reasons why. The quick and dirty answer is that those in power are lying—but let us elaborate so that you can better protect yourself financially from the lies.

The Fed has been running off its balance sheet, reducing its holdings of Treasuries and mortgage-backed securities (MBS) since about April 2022, a process identified by the euphemism “Quantitative Tightening,” or QT.

While this reduces inflationary pressure in the economy, it also reduces demand for Treasuries, making it harder for the government to borrow, at least at low interest rates. However, politicians are fond of a compliant Fed, and QT stops the free money spigot on which big-spending politicians rely.

But the Fed has taken several measures to keep the gravy train coming for politicians. In the summer of last year, it “tapered” QT, meaning it reduced the pace at which it was running down its Treasury holdings. But it continued selling off its agency debt at the previous pace, so MBS kept declining just as before.

That rationale here was that the Fed didn’t want to make Treasury markets feel the pain. Instead, it decided to put the screws to home lending and let the mortgage market bear an increasingly large portion of QT. This is not the only reason for the housing market being frozen over, but it’s certainly not helping.

But we need to understand how the Fed actually reduces its balance sheet. Does it sell the assets on the books, or simply let them mature? It does both, depending on the circumstances.

The Fed is trying to reduce its assets at a specific pace, but the maturity schedule of its holdings doesn’t usually line up perfectly with that monthly tempo. Sometimes more debt matures than necessary, and other times not enough.

When more than enough debt matures, some of the proceeds are rolled over into new debt, resulting in a purchase. When not enough debt matures, additional assets on the balance sheet are sold in the open market.

Why is this important? Because the Fed has $818 billion in unrealized losses, and that’s above and beyond the nearly-$250 billion in realized losses already accrued (mostly from interest payments to financial institutions). Whenever the Fed sells devalued assets, those debt instruments are sold below par, and the Fed realizes a loss.

But note that a loss for the Fed in this instance is effectively adding liquidity to the market, though it’s hidden by an accounting trick.

While the Fed has certain financial regulations that force banks to use mark-to-market accounting on some assets, the Fed (conveniently for itself) uses face value accounting. That means all the Treasury bonds the Fed bought with 2% yields are still counted at par, despite absolutely no one today being willing to pay anywhere near that for those assets.

So, what does this look like in practical terms? Let’s throw some numbers out to illustrate the shady three-card Monty in action.

Imagine the Fed has securities with a face value of $10 million and it sells these on the open market. Because interest rates are much higher now than when the Fed acquired those securities, no one is willing to pay the face value, and the securities sell at a steep discount of $7 million. The Fed records the transaction as reducing the balance sheet by $10 million, but it has only removed $7 million of liquidity from the market, despite having originally added $10 million at the time of purchase.

We’re not back to square one; we’re up $3 million.

Recall that when the Fed sells an asset, you give the Fed money and the Fed hands over a debt instrument, like a Treasury bond. The money you give the Fed simply vanishes; it’s extinguished. Thus, we assume—and rightly so under normal conditions—that reductions in the balance sheet are matched by reductions in liquidity.

But these aren’t normal conditions. Until the last few years, the Fed never pushed rates so low and kept them there for so long, only to raise them so quickly. The violent shifts in monetary policy over the last several years have been truly unprecedented.

Consequently, when the yields for on-the-run securities became a multiple of the yields for off-the-run securities that the Fed was selling, we stopped getting accurate feedback on the effect of QT.

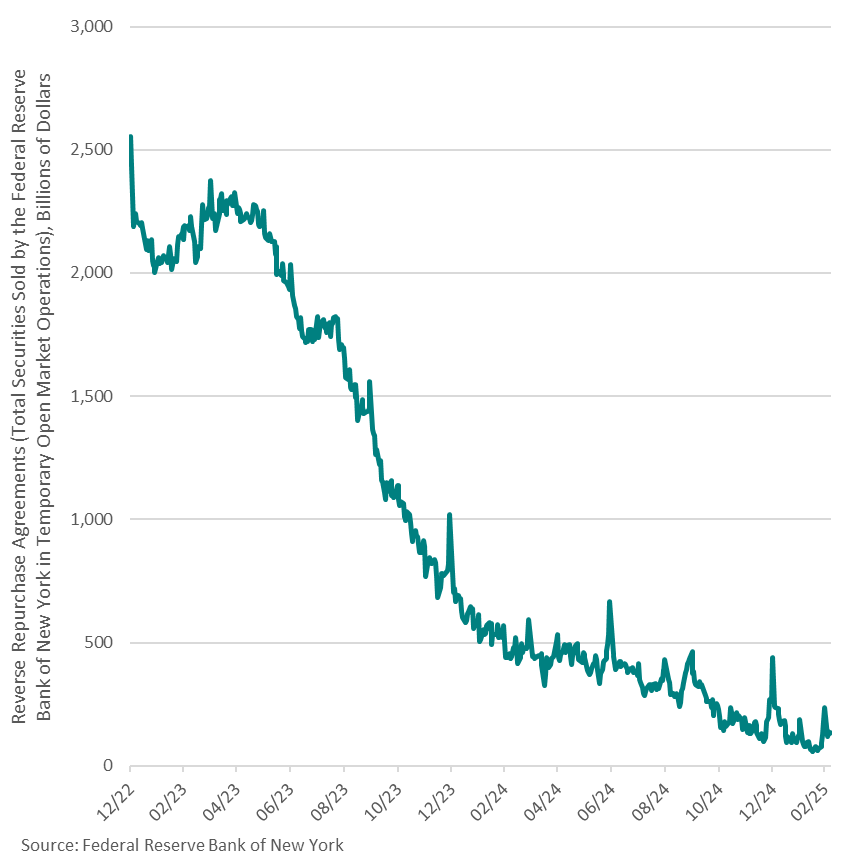

This is a big part of why the reverse repurchase agreement (RRP) facility at the Federal Reserve Bank of New York still hasn’t run dry. Theoretically, the Fed’s balance sheet has shrunk enough to bring liquidity and interest rates back into alignment, but that’s not the case once you realize the Fed hasn’t been sucking out that much liquidity at all, so it’s still working to support an interest rate floor.

(See our previous series of posts on the RRP facility for more on this mechanism and how to interpret volume, rates, etc.)

It turns out that the Fed hasn’t reined in the supply of loanable funds nearly as much as many market participants believe. More supply puts downward pressure on price, which, in this case, is the interest rate. Once again, the Fed has come to the rescue of its political masters.

But remember that price is set by supply AND demand. What we’ve seen over the last several months has been a flatlining of demand, and even a lessening to some extent.

It all has to do with the debt ceiling. Mostly.

Once this limit on government borrowing bit at the start of the year, the ever-growing appetite of the Treasury for borrowing, including for short-term loans like T-bills, was instantly satiated. Since Treasury can now only roll over existing debt, gross issuance is limited to exactly whatever is maturing. Net debt issuance has been zero for a couple of months now.

Since the RRP facility is a respite for cash and not a way to lock up liquidity for any appreciable length of time (we’re talking overnight loans here), it’s impacted much more by Treasury bills than notes or bonds. T-bills have a maximum maturity of 52 weeks with the shortest term being only a few weeks’ duration.

As former Treasury Secretary Yellen shifted Treasury issuance into a heavy reliance on T-bills to manipulate the yield curve, RRP volumes collapsed, falling from $2.5 trillion to near zero. But with Treasury up against the debt ceiling, that trend has ended.

In fact, it’s starting to reverse because the new Secretary, Bessent, is normalizing the Treasury’s maturation schedule, meaning he’s restoring the regular mix of T-bills, T-notes, and T-bonds.

As old debt matures today and is rolled over into new debt (remember this is just gross issuance since net issuance is still zero), Bessent is replacing some T-bills with longer-dated debt instruments. This is creating a net reduction in T-bills outstanding.

So, demand has decreased at the same time supply has increased, or at least supply is decreasing much slower than previously believed. Even with a 100-basis-point drop in the Fed’s target interest rate, the RRP facility still hasn’t completely drained, and the standing repo facility is, well, just standing there, doing nothing.

The effect here is hardly benign. Each month since the Fed began cutting interest rates has seen annual inflation rates ticking higher. Even if this second Trump administration can drastically cut government spending and balance the federal budget in short order, there is still a tremendous amount of inflation already baked into this cake.

Furthermore, these manipulations by the Fed, whether active maneuvers like paying interest on reserve balances and RRP operations, or passive ploys like accounting tricks, each starve the private market of capital to one degree or another, while providing money for the government to spend.

Wall Street, of course, still gets paid. The Fed is shelling out $473 million per day in interest payments to major financial firms, but the interest rates on your credit cards are at a record high, while car loans and mortgages are prohibitively expensive for many families.

This means we’re not out of the woods on inflation—not by a long shot. We were never trending toward the Fed’s 2.0% target, and now you know why.

Powell & Co. never had any intention of getting us there…