How Did The Bank's Money Disappear?

How the Fed's published data is misleading the public about small banks

Just a couple days ago, the Fed released their usual weekly data on banks and there was a massive surprise: cash at small banks exploded by 23% in just 7 days. The problem? It’s a lie.

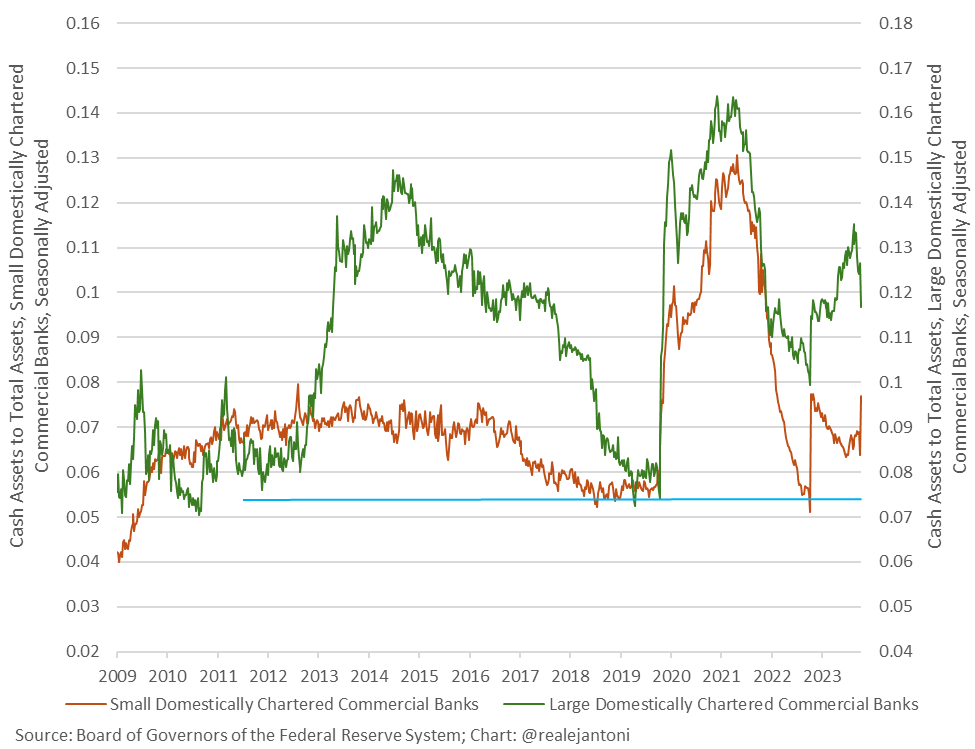

Ever since the bank collapses of last year, we’ve been watching like hawks not only the amount of cash at banks, but also the ratios of cash to other parts of their balance sheet, and the data has been telling an interesting story.

Small banks used the Bank Term Funding Program over the last year to build up cash reserves. That allowed these banks to have an adequate amount of cash assets relative to deposits.

That’s important because if their cash-to-deposits runs too low, they end up having to liquidate assets—and fast—to raise the cash that depositors want to withdraw.

Alternatively, those banks would need to borrow cash from better capitalized banks and pay interest at the Fed Funds rate, which is higher than the interest they’re receiving on a lot of their assets.

The cash raised from the BTFP also allowed small banks to have sufficient cash assets relative to their total assets, preventing them from becoming cash reserve constrained.

So that brings us to the last week of the BTFP, when cash supposedly poured into small banks at an astronomical 23% in a single week, while cash fled large banks, dropping 8%.

Our initial reaction was that small banks had one last hurrah at the emergency lending facility and raised a ton of cash as a safety backstop in these uncertain times. Since the BTFP loans have no prepayment penalties, there’s not much risk to such a strategy.

Conversely, we thought the New York Community Bancorp mess likely caused the drop in cash at big banks.

But that’s not what happened. In fact, small bank cash didn’t increase at all.