Bleak Outlook Even Through Rose-Tinted Glasses

CBO's overly optimistic projections are still horrific

This past week, the Congressional Budget Office released their latest projections, and the results aren’t good. But the much more worrying part is that the CBO assume a best-case scenario - something that never, ever materializes.

The reality that we’re facing is much worse.

We’re not saying this because we like to be the bearer of bad news. Rather, the more you know, the better you can protect yourself (and your portfolio) from what’s coming down the pike.

Let’s start with some of the assumptions *cough, wishful thinking, cough* that CBO has built into their so-called model over the next decade:

unemployment rate tops out at 4.4% this year then remains low

inflation is down to 2% this year and falls further within 5 years

200 basis points of interest rate cuts in the next 10 months alone

continued flood of “immigration” adding $7 trillion to GDP

reduction in the impact of increased borrowing on interest rates

deficit of only $1.6 trillion this fiscal year

no recession - ever

There’s more ridiculousness, but we’ll pause here so that you can get all the laughs out of your system.

Let’s start with the deficit since we’ve talked about that extensively. Yellen’s Treasury has already borrowed $1.02 trillion in the first 4 months of this fiscal year and still has 8 to go. The idea that we’ll borrow half as much over twice as many months is beyond parody.

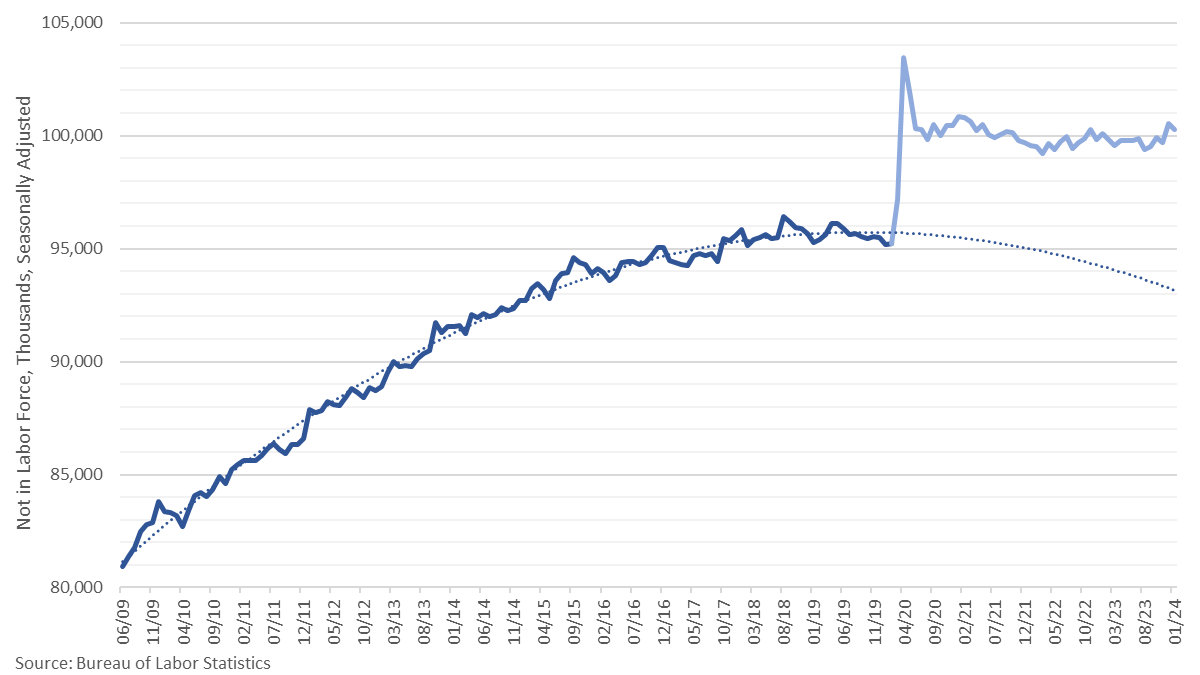

On the unemployment rate front, an honest assessment of the numbers shows the CBO is already wrong. The Bureau of Labor Statistics, who publishes the official unemployment rate, also has data showing how many people are not in the labor force.

That category predictably spiked during the government-imposed lockdowns of 2020, but never returned to its pre-pandemic level, let alone its pre-pandemic trend, which was downward during the booming economy of 2019 through February 2020.

These are people who are unemployed but are not counted as such, nor are they included as part of the labor force. If we add those people back into the calculation, we get an unemployment rate over 6%.

That’s in line with other estimates derived from trends in the employment-to-population ratio, the employment level, and the number of nonfarm payrolls. A more accurate unemployment rate is somewhere between 6.3% and 7.4%.

Clearly, the CBO’s estimate of an unemployment rate maxing out at 4.4% is hogwash.

And there’s no reason to trust the inflation projections from CBO or anyone else who was on Team Transitory, or who claimed inflation was just a function of supply-chain disruptions. Enough said there.

On interest rate cuts, the CBO might not be far off from the truth. We’ve previously explained that Powell & Co. are going to cut as many times this year as they can get away with. Even still, that incentive only exists before the November election.

That means we’re not looking at 200bps in cuts over 10 months, but only 8 months. That’s a tall order, but we’ll admit there’s a chance Powell & Co. make it happen.

However, fulfilling that assumption means contradicting another one: inflation.

Flooding the economy with liquidity again will set off another inflationary storm, and that throws the CBO assumption of low inflation right out the window. You can’t have your cake and eat it too.

Next is this risible labor force projection, based on a continued flood of illegals pouring through the southern border. The crazy bean counters at CBO are literally assuming that the “migrants” will all go to work, none will get on welfare or other assistance, and it’ll make the labor market go to the moon.

(In hindsight, we should’ve put a warning on this post to make sure you were sitting down before you started reading…)

Believing that an endless supply of cheap labor will add indefinitely to an economy, the CBO has tacked on $7 trillion in additional economic growth over the next 10 years. It’s like magic!

Then there’s the lunacy of borrowing more having less of an impact on interest rates.

What we’ve seen over the last 4 years is that everything has a breaking point, including bond markets. Modern Monetary Theory is completely wrong - government borrowing always has an impact, the magnitude of which increases as the deficit grows.

The bond vigilantes will always have their day.

Apparently, the lesson the CBO learned from this is that if we only borrow more money, interest rates won’t rise as much. Yes, you read that right: if we increase the demand for loanable funds, the price of loanable funds is impacted less.

Ladies and gentlemen, the inmates are truly running the asylum.

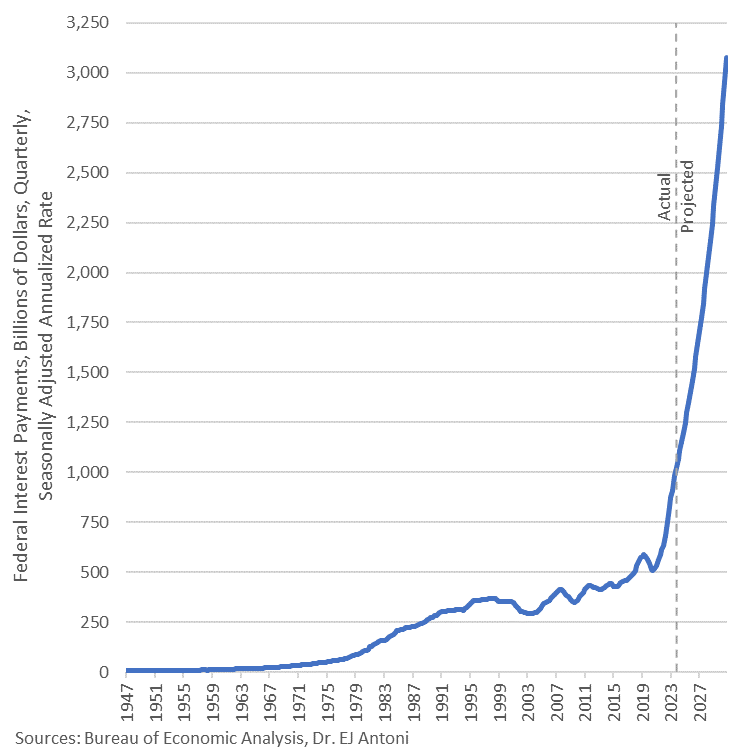

That small tweak reduces the projected interest on the debt by hundreds of billions of dollars, when it should be rising by hundreds of billions. That, in turn, reduces the projected deficit.

More realistic estimates have interest on the debt going to an annualized $3 trillion by the fourth quarter of 2030:

Lastly, there’s the children’s bedtime story happy ending of no recessions ever again.

During a downturn, government revenues tank and outlays explode as economic activity results in less tax revenue and joblessness lets more people live on the dole. CBO blissfully assumes away such real-world possibilities. Must be nice.

Meanwhile, the report makes no mention of the ongoing banking crisis, the commercial real estate disaster, the sharp drop in federal tax receipts over the last few years, the equity bubble, etc.

So, where does that leave us? Slightly more informed, believe it or not.

Politicians will cite this report as evidence that we don’t need to drastically cut spending and borrowing, or even printing of money, to fund the bloat in DC. The Fed will err on the side of easy money and more inflation, while economic growth will be lackluster.

But this doesn’t mean things like equities or home prices will flatline. Recall that these are priced in nominal terms, not real terms. Having your money in places where prices appreciate with inflation helps minimize your losses.

Likewise, less-informed investors who buy into these ludicrous CBO figures will probably underprice inflation-protected securities, like TIPS or I-bonds. (We detailed before how we like to time the purchase of these assets.)

When it comes to investing and hedging, knowing what’s coming can often be more valuable than being surprised by good news. There are a plethora of financial instruments today (especially swaps) that provide the opportunity for positive returns in virtually any economic landscape, even deeply negative ones.

We don’t want to see the nation go further down the road to economic oblivion, which is why we like to promote sound fiscal and monetary policies. But we also see no reason to go with the crowd and let ourselves be sheered like the rest of the sheep by believing these crazy government projections.

Sometimes you have to bet against your favorite sports team - not because you’re disloyal - but because the numbers tell you to.

Here’s hoping America gets back to winning soon.

Great stuff.!

https://twitter.com/hussmanjp/status/1754862551509127543?t=PEw9JV25WvOniNBoI75dag&s=19